Running a growing company comes with a frustrating challenge: managing cash flow when clients take their time to pay. You deliver excellent work, send out the invoice, and then the waiting game begins. Waiting 30, 60, or even 90 days for payments can cripple your ability to buy inventory, cover payroll, or take on new projects. This gap between billing and getting paid is a massive problem that keeps owners awake at night, wondering how they will fund their daily operations while their money is tied up in accounts receivable.

Fortunately, there is a proven solution to unlock that trapped capital quickly. By selling your outstanding invoices to a third-party financing company, you can get an immediate cash injection. If you are considering this path, understanding the average invoice factoring rates for small business is your crucial first step. Knowing exactly what these financing companies charge allows you to make an informed decision, protect your profit margins, and secure the best possible deal to keep your operations running smoothly without taking on traditional debt.

What Are the Average Invoice Factoring Rates for Small Business?

When you decide to finance your receivables, the primary cost you will encounter is the factor fee, also known as the discount rate. Generally speaking, the average invoice factoring rates for small business fall between 1.5% and 5.0% of the total invoice value. This percentage is deducted from the final payout you receive once your client settles their bill.

However, viewing that 1.5% to 5.0% range in a vacuum can be slightly misleading. The exact rate you receive depends entirely on your specific circumstances, your industry, and the financial health of the clients you are billing. A highly established B2B service provider might secure a rate closer to 1.5%, while a newer commercial contractor might see rates closer to 3.5% or 4.0%.

It is also important to distinguish the factoring rate from the advance rate. The advance rate is the percentage of the invoice the company gives you upfront on day one. This usually ranges from 80% to 95%. The remaining 5% to 20% is held in a reserve account. Once your client pays the full invoice, the financing provider takes their fee from that reserve and returns the rest to you. Therefore, the average invoice factoring rates for small business dictate how much money you actually pay for the service, while the advance rate dictates your immediate day-one cash flow.

How Do Finance Companies Calculate These Rates?

Understanding the math behind the average invoice factoring rates for small business helps you accurately forecast your costs. Factoring providers generally use one of two main pricing models: flat-rate structures and variable (or tiered) rate structures.

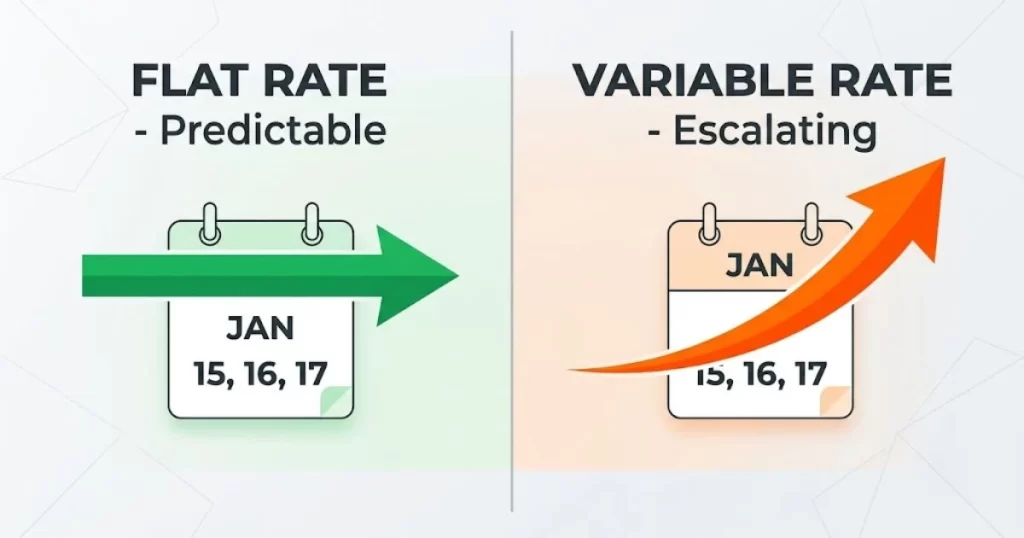

The Flat-Rate Pricing Model

Under a flat-rate model, you agree to a single, fixed percentage fee for the entire time the invoice is outstanding, up to a certain limit (usually 60 to 90 days). For example, a provider might offer a flat 2.5% fee on a net-30 invoice.

Whether your client pays on day 12 or day 29, you pay exactly 2.5%. This model offers incredible predictability. It makes budgeting highly straightforward because you know your exact cost the moment you submit the invoice. Many owners prefer flat structures when trying to lock in the best average invoice factoring rates for small business because it removes the anxiety of late-paying customers.

The Variable (Tiered) Rate Model

The variable rate structure is highly common and works like a meter running over time. You might be charged a base rate of 1.5% for the first 30 days. After that, the provider might charge an additional 0.5% for every 10 or 15 days the invoice remains unpaid.

If your customer pays on day 25, you only pay the initial 1.5%. But if they drag their feet and pay on day 55, your total fee climbs to 2.5% or more. This structure can offer the lowest average invoice factoring rates for small business if you have clients who consistently pay early. However, it can become very expensive if your customers habitually stretch their payment terms past the due date.

Key Elements Influencing Average Invoice Factoring Rates for Small Business

You might wonder why one company pays 1.5% while another pays 4.5%. Providers do not pull these numbers out of thin air. They base their quotes on a strict risk assessment. Here are the primary factors that move the needle on the average invoice factoring rates for small business.

Customer Creditworthiness

In traditional banking, your personal and business credit scores dictate your loan terms. In factoring, the focus flips completely to your customers. The financing company is relying on your clients to pay the bill, so they assess your clients’ credit history and financial stability.

If you are billing Fortune 500 companies, government agencies, or large hospital systems, the risk of non-payment is practically zero. Because the risk is low, you will be offered the most competitive average invoice factoring rates for small business. If your clients are small independent shops with spotty credit histories, the provider takes on more risk and will charge a higher percentage.

Monthly Invoice Volume

Volume is a massive pricing lever in the commercial finance world. Factoring providers prefer to work with businesses that have a high volume of receivables. Processing a single $100,000 invoice requires roughly the same administrative work as processing a $10,000 invoice, but the payout for the provider is much larger.

Therefore, companies committing to factoring $250,000 or more per month will almost always secure lower average invoice factoring rates for small business compared to a company only factoring $20,000 a month. By guaranteeing more revenue for the provider, you earn volume discounts that directly improve your bottom line.

Payment Terms and Invoice Aging

Time equals risk in the financial sector. The longer capital is deployed, the more it costs. If your standard billing terms are Net-30, the provider knows they will get their money back relatively fast.

Conversely, if you offer Net-60 or Net-90 terms, the financing company’s capital is tied up for months. Longer payment windows naturally lead to higher average invoice factoring rates for small business. Providers will closely review your Accounts Receivable aging report to see how long your clients typically take to actually send the check.

Industry-Specific Average Invoice Factoring Rates for Small Business

The industry you operate in plays a surprisingly large role in the quotes you receive. Some sectors have predictable, straightforward billing practices, while others involve complex progress payments that introduce higher risks. Here is a breakdown of the typical average invoice factoring rates for small business across different industries.

Trucking and Freight

The transportation sector relies heavily on factoring to cover daily fuel and maintenance costs. Because the billing process (involving rate cons and bills of lading) is highly standardized, risk is moderate. The average invoice factoring rates for small business in trucking generally range from 1.5% to 3.5%. Many freight factors also offer high advance rates, sometimes up to 95% or even 100%, because the turnaround time on freight bills is usually quite fast.

Staffing Agencies

Staffing firms constantly battle payroll demands while waiting for corporate clients to settle invoices. Since staffing invoices are usually recurring and often billed to larger, stable companies, factors love this industry. The average invoice factoring rates for small business in the staffing sector are highly competitive, typically sitting between 1.5% and 3.5%.

Construction and Contracting

Construction financing is notoriously difficult. Invoices often involve progress billing, “pay-when-paid” clauses, and the constant threat of mechanic’s liens. Because disputes over completed work are common, factors view construction as a high-risk category. Consequently, the average invoice factoring rates for small business in construction are higher, usually falling between 2.5% and 5.0%, with lower advance rates around 70% to 80%.

B2B Services and Manufacturing

For general B2B services, IT consulting, and manufacturing, rates fall firmly in the middle. The cost depends entirely on the supply chain stability and client quality. For these sectors, the average invoice factoring rates for small business generally hover around 1.5% to 3.5%.

Recourse vs. Non-Recourse: Which Offers Better Rates?

When negotiating your contract, you will have to choose between recourse and non-recourse agreements. This legal distinction dramatically impacts the average invoice factoring rates for small business you will pay.

Recourse Factoring

Recourse factoring is the most common arrangement, making up roughly 80% of the US market. In a recourse agreement, you remain ultimately responsible if your client fails to pay. If a customer goes bankrupt or simply refuses to pay a factored invoice after 90 days, you must buy that invoice back from the factoring company or swap it for a new, valid invoice.

Because the provider takes on less risk, recourse agreements offer the lowest average invoice factoring rates for small business. You can typically expect fees to be 0.5% to 1.5% cheaper per invoice compared to non-recourse options. This is the ideal choice if you completely trust your clients’ ability to pay.

Non-Recourse Factoring

Non-recourse factoring offers a safety net. Under this structure, the factoring company absorbs the credit loss if your customer becomes formally insolvent or goes bankrupt. You do not have to buy the invoice back if the client goes out of business.

However, this protection comes at a premium price. Because the provider acts as a quasi-credit insurance agency, they charge higher average invoice factoring rates for small business. Furthermore, it is vital to read the fine print. Non-recourse only protects against formal bankruptcy, not late payments or customer disputes over the quality of your work.

Hidden Fees to Watch Out For Beyond the Basic Rate

When shopping for financial partners, looking solely at the headline discount fee is a dangerous mistake. Many providers advertise incredibly low average invoice factoring rates for small business, only to pad their profits with hidden ancillary charges. To understand your true cost of capital, you must ask about the following fees.

Origination and Setup Fees

Just like a traditional bank loan, many providers charge a fee simply to open your account. This covers the cost of running credit checks on your customers and setting up the legal framework. Setup fees can range from zero to several hundred dollars. Always negotiate to have these waived when discussing the average invoice factoring rates for small business with a new provider.

Monthly Minimum Volume Penalties

This is the most critical clause in your contract. Many agreements require you to factor a specific minimum dollar amount every single month (e.g., $50,000 minimum). If your sales dip in a slow month and you only factor $30,000, you will be hit with a hefty shortfall penalty. When evaluating the average invoice factoring rates for small business, ensure any volume minimums align perfectly with your most conservative sales projections.

ACH, Wire, and Processing Fees

How does the money physically get to your bank account? Providers often charge $15 to $30 for every wire transfer they send you. While this sounds small, if you fund invoices three times a week, wire fees can add thousands of dollars to your annual expenses. Additionally, some companies charge a flat $10 to $25 processing fee per invoice. These micro-charges artificially inflate the true average invoice factoring rates for small business.

Lockbox and Maintenance Fees

When you factor invoices, your clients send their payments directly to a secure lockbox managed by the factoring company. Some providers charge a monthly maintenance fee to manage this lockbox and perform collection duties. Always ask if administrative tasks are included in the base average invoice factoring rates for small business or billed separately as line items.

Real-World Example: Calculating Your True Costs

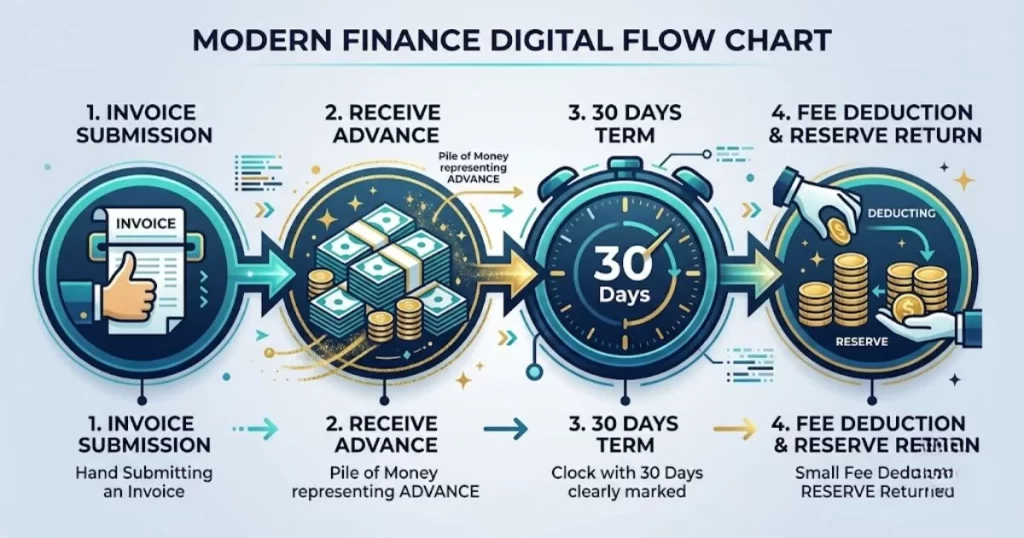

To truly grasp the average invoice factoring rates for small business, it helps to walk through a concrete, real-world math example. Let us imagine you run a commercial cleaning business and you want to factor a $50,000 invoice with a Net-30 payment term.

Assume the provider offers you an 85% advance rate and a flat factoring fee of 2.5% for 30 days.

- Step 1: The Advance. You submit the $50,000 invoice. The provider immediately wires you 85%, which is $42,500. You now have cash to make payroll.

- Step 2: The Reserve. The remaining 15% ($7,500) is held in the provider’s reserve account.

- Step 3: The Client Pays. Thirty days later, your client pays the full $50,000 directly to the factoring company.

- Step 4: The Fee Deduction. The provider calculates their 2.5% fee based on the total invoice value. 2.5% of $50,000 is $1,250.

- Step 5: The Final Payout. The provider takes their $1,250 fee from the $7,500 reserve. They then wire you the remaining $6,250.

In this scenario, your total cost to access $42,500 a month early was $1,250. This perfectly illustrates how the average invoice factoring rates for small business directly impact your profit margin on a per-project basis.

How Invoice Factoring Compares to Traditional Bank Loans

Many owners wonder if they should just go to a local bank instead of worrying about the average invoice factoring rates for small business. While traditional bank loans or lines of credit almost always have lower annual percentage rates (APRs), they serve very different purposes.

Speed of Funding

A traditional bank loan can take weeks or even months to underwrite. You have to submit years of tax returns, personal financial statements, and detailed business plans. Factoring, on the other hand, is incredibly fast. Once your account is set up, you can submit an invoice on Tuesday morning and have the cash in your account by Tuesday afternoon.

Credit Requirements

Banks focus heavily on the business owner’s personal credit score and the company’s historical profitability. If you are a startup or have bruised credit, a bank will likely deny you. Factoring ignores your personal credit score almost entirely. Because they look at your customers’ credit, factoring is highly accessible for new, rapidly growing businesses.

Understanding the APR Illusion

If you annualize a 3% factoring fee over a year, it translates to an APR of roughly 36%. This sounds terrible compared to a 10% bank loan. However, factoring is not a long-term loan; it is a 30-day cash advance. You only pay the fee once per invoice. When you urgently need to buy supplies to fulfill a lucrative contract, paying a flat fee to unlock your own money is often a smart business move, making the average invoice factoring rates for small business a worthwhile investment in growth.

Expert Tips on Lowering Your Factoring Costs

You do not have to accept the first quote a provider hands you. Financial consultants frequently help companies negotiate better terms. Here are proven strategies to secure the lowest average invoice factoring rates for small business.

1. Leverage Your Best Customers

“The easiest way to drop your rates is to selectively factor only your strongest accounts,” notes a leading commercial finance advisor. “If you have five clients, and two of them are massive, publicly traded corporations, only submit those invoices. The factor will see the pristine credit risk and offer you the most aggressive average invoice factoring rates for small business possible.”

2. Push for Higher Volumes

If you know your sales are going to trend upward, use that as leverage. Tell the provider you plan to push all your receivables through their facility. By committing a higher monthly volume, you move into a better pricing tier. Just ensure you can actually hit those targets to avoid minimum volume penalties.

3. Improve Your Internal Collections

If you opt for a variable rate structure, the speed at which your clients pay dictates your cost. You can lower your average invoice factoring rates for small business simply by communicating better with your clients. Send polite payment reminders before the due date. The faster the check arrives at the lockbox, the less you pay in tiered factoring fees.

4. Shop Around and Compare Quotes

Never settle for a single proposal. The alternative finance market is highly competitive. Get quotes from at least three different companies. Show the competing offers to your preferred provider. Factoring companies want your business, and they will frequently match a competitor’s offer to give you the best average invoice factoring rates for small business.

Spot Factoring vs. Whole-Ledger Factoring

The type of contract you sign also changes your pricing structure. You generally have two choices: factoring your whole ledger or spot factoring.

Whole-Ledger Agreements

In a whole-ledger arrangement, you agree to submit every single invoice you generate to the factoring company. Because you are handing over maximum volume, the provider gives you massive discounts. This is where you find the absolute lowest average invoice factoring rates for small business. The downside is a loss of flexibility, as you must finance invoices even when you do not strictly need the cash.

Spot Factoring

Spot factoring allows you to pick and choose individual invoices. If you only need cash in December to cover holiday bonuses, you can factor just one $20,000 invoice and leave the rest alone. The ultimate flexibility is fantastic, but it comes at a cost. Because the volume is low and sporadic, spot factoring carries significantly higher average invoice factoring rates for small business, often pushing past 3.5% or 4.0% per invoice.

How to Choose the Right Factoring Company for Your Small Business

Finding the right financial partner is about more than just hunting for the lowest average invoice factoring rates for small business. A bad factoring company can ruin your relationships with your clients through aggressive collection tactics. Keep these criteria in mind during your search.

Industry Expertise

Choose a provider that understands your specific sector. A factor that specializes in trucking understands fuel advances and bill of lading documents. A medical factor understands Medicare and insurance payouts. Industry specialists process paperwork faster and offer more accurate average invoice factoring rates for small business tailored to your typical payment cycles.

Transparent Customer Service

You will be interacting with this company weekly. You need an account manager who answers the phone. Ask current clients about their experience. If the factor is difficult to reach or provides confusing accounting reports, the headaches will outweigh any savings you got from low average invoice factoring rates for small business.

Client Communication Policies

Remember, the factoring company will be collecting money directly from your customers. You must ask how they handle this. Do they act as a seamless extension of your billing department, or are they aggressive debt collectors? You want a partner who maintains a professional, courteous tone so your clients never feel harassed.

The Impact of Economic Conditions on Factoring Rates

It is crucial to recognize that commercial finance does not exist in a vacuum. Broader macroeconomic trends deeply impact the average invoice factoring rates for small business. Factoring companies borrow their capital from larger banks to fund your advances.

When central banks raise baseline interest rates to combat inflation, the cost of capital goes up for everyone. Factoring companies pass these increased borrowing costs down to you. Therefore, in a high-interest-rate economic environment, you will naturally see the average invoice factoring rates for small business creep upward across the entire industry. Conversely, when the economy is booming and interest rates drop, factoring becomes cheaper.

Staying aware of current economic conditions helps you know whether a quoted rate is genuinely fair or artificially inflated. If the national base rates are high, expecting a 1% factoring fee is unrealistic. Adjusting your expectations based on the broader financial market ensures you can accurately evaluate the average invoice factoring rates for small business in any given year.

Factoring as a Growth Strategy, Not Just a Lifeline

Historically, some viewed factoring as a last resort for failing companies. Today, that stigma is entirely gone. Smart, highly profitable companies actively seek out the best average invoice factoring rates for small business to fuel aggressive growth.

Imagine you are offered a massive contract that will double your revenue, but it requires hiring five new employees immediately. You cannot wait 60 days for the first invoice to clear to pay those new hires. By utilizing an invoice factoring facility, you instantly turn your accounts receivable into liquid cash, allowing you to scale without giving up equity to investors or taking on restrictive bank loans.

When viewed as a tool for expansion, paying the average invoice factoring rates for small business becomes a simple operational expense that unlocks massive new revenue streams. The cost of the factor fee is easily eclipsed by the profit generated from the new business you were able to accept.

Frequently Asked Questions (FAQs)

To summarize the complexities of commercial finance, here are the most common questions owners ask when researching cash flow solutions.

What exactly are the average invoice factoring rates for small business right now?

In 2026, you can generally expect fees to range from 1.5% to 4.0% per 30-day period. This depends heavily on your industry, monthly volume, and your clients’ credit history.

Are the average invoice factoring rates for small business higher than a traditional bank loan?

Yes, if you calculate the APR, factoring is more expensive. However, factoring is easier to qualify for, provides cash in 24 hours, and does not create debt on your balance sheet, making it ideal for short-term working capital needs.

How can I negotiate the lowest average invoice factoring rates for small business?

The best way to lower your rate is to commit to a higher monthly factoring volume, choose recourse factoring, and only factor invoices from your most creditworthy, reliable customers.

Do average invoice factoring rates for small business include hidden fees?

They often do not. The headline rate is just the start. You must always ask the provider about setup fees, wire transfer fees, lockbox fees, and monthly minimum volume penalties to understand your true cost.

Does my personal credit score affect my average invoice factoring rates for small business?

Rarely. While a factor might run a soft background check for fraud prevention, they base their pricing and approval almost entirely on the credit scores and payment history of the customers you are billing.

Conclusion

Managing cash flow is the lifeblood of any growing enterprise. When slow-paying clients threaten to stall your operations, leveraging your accounts receivable is a fast, reliable, and highly effective strategy to regain financial control. By thoroughly understanding the average invoice factoring rates for small business, you empower yourself to navigate the commercial finance market with absolute confidence.

Remember that the cheapest headline rate is not always the best deal. You must weigh the flat fees versus variable rates, understand the impact of recourse vs. non-recourse contracts, and aggressively hunt for hidden ancillary costs in the fine print. By applying the strategies outlined in this guide—from leveraging your strongest clients to negotiating volume discounts—you can successfully secure the most favorable average invoice factoring rates for small business available in today’s market. With the right financial partner and a transparent fee structure, you can stop worrying about when the next check will arrive and get back to focusing on what you do best: growing your company.

Ready to unlock your cash flow and scale your operations without the wait?

Do not let outstanding invoices hold your growth back for another day. If you want personalized advice on securing the best financing terms, visit our Contact Us page today. Our team is ready to analyze your receivables and help you secure the lowest average invoice factoring rates for small business tailored specifically to your unique needs! Reach out now and get funded within 24 hours.