Waiting 30, 60, or even 90 days for B2B customers to pay their invoices can throttle your business growth. When cash is tied up in unpaid bills, meeting payroll, buying inventory, or taking on new contracts becomes an uphill battle. Many business owners turn to invoice financing to bridge this gap, but choosing the wrong structure can lead to unexpected financial liabilities.

To make the right choice for your company, you need to have non recourse vs recourse factoring explained in clear, simple terms. The fundamental difference lies in who carries the ultimate financial risk if your customer defaults on their bill. Having non recourse vs recourse factoring explained helps you see that while one option shields you from bad debt, the other offers lower fees and higher approval rates. Let’s break down how these two options work, their pros and cons, and how to choose the best path for your cash flow needs.

What is Invoice Factoring? A Quick Refresher

Before looking at the two main types, let’s establish exactly how invoice factoring operates. Factoring is not a loan; it is the sale of an asset. You sell your outstanding commercial invoices to a financial company, known as a factor, at a slight discount.

The factor advances you a significant portion of the invoice value immediately, usually between 80% and 95%. Once your customer pays the factor the full amount, the factor releases the remaining balance to you, minus a small processing fee. This mechanism injects immediate working capital into your business without taking on traditional debt.

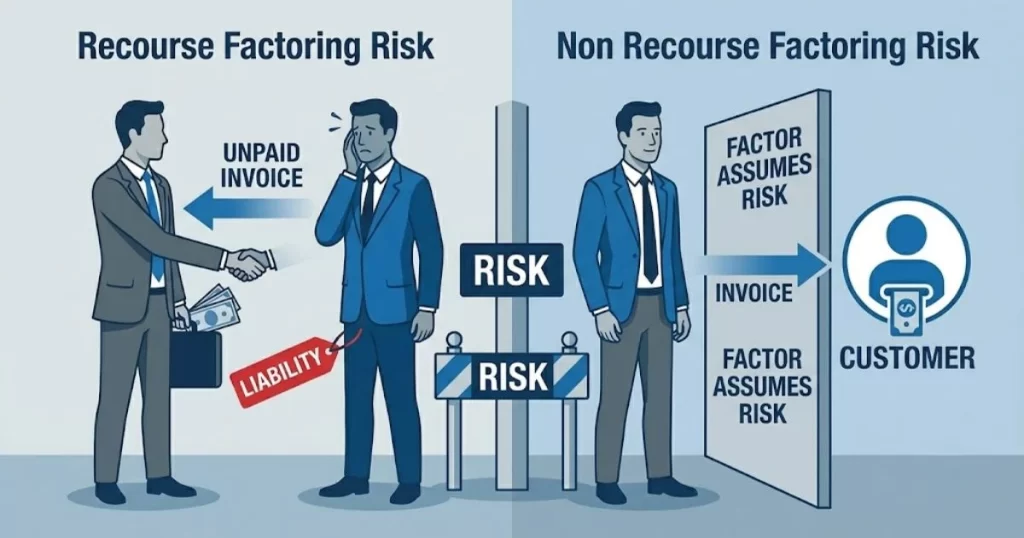

Understanding Recourse Factoring

Recourse factoring is the most common and widely available form of invoice financing. In this setup, your business retains the ultimate responsibility for the invoices you sell. If your customer fails to pay the factor within a structured timeframe, you must buy that invoice back.

How Recourse Factoring Works in Practice

When you submit an invoice under a recourse agreement, the factor advances the cash based on the assumption that the customer is trustworthy. However, if that customer runs into financial trouble, disputes the invoice, or simply refuses to pay after 60 or 90 days, the factor will trigger the recourse clause.

At that point, your company must resolve the balance. You can do this by either replacing the unpaid invoice with a fresh, valid invoice of equal value, or by having the factor deduct the money directly from your reserve account or future cash advances.

The Major Benefits of Recourse Factoring

- Lower Fees: Because you are retaining the credit risk, the factoring company takes on less danger. Consequently, they charge significantly lower discount fees and administrative rates.

- Higher Advance Rates: Factors are often willing to advance a larger percentage of the total invoice value upfront because they know their money is secure.

- Easier Approval: If your business or your customers have less-than-perfect credit scores, recourse factoring is much easier to qualify for because your company acts as the ultimate guarantor.

The Drawbacks to Keep in Mind

The main downside is the lingering financial liability. If you operate in an industry with high default rates, a single large unpaid invoice could disrupt your cash flow balance when the factor demands repayment. It requires you to maintain a cash cushion to handle potential customer defaults.

Understanding Non Recourse Factoring

Non recourse factoring offers a layer of credit protection for your business. In this arrangement, the factoring company assumes the financial risk of non-payment for the invoices they purchase from you. If the customer goes bankrupt, the factor absorbs the loss.

The True Meaning of “Non Recourse”

It is vital to understand that non recourse factoring is not a blanket insurance policy for all unpaid bills. The factor only absorbs the loss if the non-payment is caused by documented financial insolvency or bankruptcy.

If your customer refuses to pay because of a dispute over quality, late delivery, or a breach of contract, the non recourse clause does not apply. In those scenarios, the factor will pass the invoice back to you, just like in a recourse agreement.

Why Businesses Choose Non Recourse Agreements

- Bad Debt Protection: It functions as built-in credit insurance against catastrophic customer bankruptcies.

- Predictable Balance Sheets: You can comfortably remove the sold invoices from your accounts receivable without worrying about unexpected liability claims down the road.

- Peace of Mind: It allows business owners to extend credit terms to larger clients without risking the foundational stability of their own operation.

The Trade-offs of Going Non Recourse

- Premium Pricing: Security comes at a price. Factors charge notably higher fee structures to cover the cost of credit risk management.

- Stringent Credit Checks: The factor will heavily scrutinize your customers’ financial histories. They will easily reject invoices from clients who do not possess stellar credit ratings.

- Lower Advance Percentages: To further mitigate their exposure, factoring firms might hold back a larger reserve percentage, giving you less cash upfront.

Non Recourse vs Recourse Factoring Explained: Side-by-Side Comparison

To help you visualize how these two financial structures stack up against each other, review this breakdown of their key features:

| Feature | Recourse Factoring | Non Recourse Factoring |

| Ultimate Credit Risk | Retained by your business | Assumed by the factoring company |

| Triggers for Return | Any non-payment or dispute | Disputes only (Insolvency is protected) |

| Cost & Service Fees | Lower (typically 1% to 3%) | Higher (typically 3% to 5%+) |

| Approval Difficulty | Moderate; accessible to most | High; requires creditworthy clients |

| Advance Rates | Higher (up to 95%) | Lower (typically 80% to 85%) |

| Impact on Balance Sheet | Contingent liability remains | True sale; removes asset risk |

Real-World Scenarios: Which One Fits Your Business?

Choosing between these options depends on your specific industry, your clients’ financial strength, and your risk tolerance. Let’s look at two practical examples to see how these choices play out.

Scenario A: The Manufacturing Supply Chain

Imagine you run a commercial packaging business. You regularly sell large orders to well-established, publicly traded consumer brands. These brands have strong credit profiles, but they demand strict 90-day payment windows.

In this scenario, recourse factoring is usually the smarter choice. Because your clients are financially rock-solid, the actual risk of bankruptcy is incredibly low. Choosing recourse allows you to secure the lowest possible fees and maximize your cash advance, without paying a premium for protection you don’t realistically need.

Scenario B: The Logistics and Trucking Sector

Now consider a regional freight brokerage firm. You work with a rotating roster of independent shippers, mid-sized distributors, and newer startups. Your customer base fluctuates, and you don’t always have deep visibility into their long-term financial health.

Here, non recourse factoring provides an essential safety net. If a mid-sized distributor unexpectedly closes their doors or files for reorganization, your brokerage won’t be forced to repay tens of thousands of dollars in advanced freight bills. The higher fee is a worthwhile investment to safeguard your payroll stability.

Insider Tips from Financial Experts

When negotiating with funding companies, it helps to know what to look for in the fine print. Industry consultants emphasize that transparency is the most important element of any financing relationship.

“Many business owners sign non recourse agreements thinking they are completely immune to non-payment issues,” says senior corporate trade consultant Marcus Vance. “You must read the contract definitions carefully. Always ask the factor exactly what documentation they require to prove client insolvency before they agree to waive the recourse requirement.”

Furthermore, keep an eye out for hidden administrative costs. Some factoring companies charge separate fees for credit checks, invoice processing, and wire transfers. A recourse plan with hidden fees can easily end up costing more than a transparent non recourse arrangement.

How to Evaluate a Factoring Company’s Offer

If you are ready to implement invoice financing, use this checklist to compare proposals from different financial providers:

- Examine the Recourse Period: For recourse contracts, determine exactly how many days an invoice can remain past due (usually 60 or 90 days) before the factor demands repayment.

- Verify the Credit Approval Process: For non recourse options, ask how quickly the factor approves or denies credit limits for new customers you onboard.

- Check for Minimum Volume Requirements: Ensure the provider does not penalize you if your monthly invoice volume drops during slow business seasons.

- Review the Termination Clauses: Look closely at the contract duration and any potential fees associated with switching providers or closing the account.

Conclusion: Making the Right Strategic Choice

Having non recourse vs recourse factoring explained clears up the confusion surrounding invoice financing and puts the control back in your hands. Recourse factoring serves as a cost-effective, high-advance tool for businesses working with reliable, creditworthy clients. On the flip side, non recourse factoring acts as a strategic shield, protecting your working capital from unexpected customer insolvencies at a slightly higher cost.

Take a close look at your current accounts receivable, assess the credit health of your primary clients, and determine how much risk your business can comfortably handle. By selecting the model that aligns with your operational reality, you can unlock consistent cash flow, eliminate payment delays, and fuel your long-term business growth.

If you need personalized guidance to analyze your business invoices, determine the best financing structure for your specific industry, or set up a secure funding pipeline, we are here to assist. Visit our website Contact Us page right away to speak directly with an enterprise finance specialist and secure the working capital your business deserves.